LINCOLN — The draft text of Gov. Jim Pillen’s plan to reduce Nebraska property taxes calls for new taxes on certain goods or services and phasing out most local K-12 property taxes over three years.

The Nebraska Examiner obtained the draft document and verified it over the weekend with six lawmakers who are part of a 17-member task force working with Pillen on the proposal. The outline calls for collecting more than $1 billion from the sales of currently tax-exempt goods or services, including agricultural and machinery and equipment and energy used in industry or agriculture.

“I would say that what you were sent is a very accurate depiction of kind of where we are heading,” State Sen. Mike Jacobson of North Platte said Sunday.

“You have correctly stated everything the committee has discussed. At this point the committee has not decided on a specific plan,” State Sen. Steve Erdman of Bayard said in a text.

State Sens. Teresa Ibach of Sumner, Merv Riepe of Ralston, George Dungan of Lincoln and John Fredrickson of Omaha also confirmed the Examiner’s reporting. Several stressed that the ideas remain in motion and that the group will likely meet at least once more before the expected special session begins July 25.

School funding phaseout

A major component of the Pillen-led plan is phasing out all operating expenses for K-12 public school districts, which is about 80% of some district budgets and includes teacher salaries. Instead, the state would take on that burden.

The plan states this would cost about $1.2 billion in the first year.

To accomplish that goal, lawmakers would subsidize local spending levels and phase-down current tax rates for schools, with nearly all up to $1.05 per $100 of property valuations to:

- 15 cents in 2024.

- 7.5 cents in 2025.

- 0 cents in 2026.

Property owners would receive a credit beginning on their 2025 property tax statements to reflect the lower tax rates.

Jacobson said the tax rates are still being negotiated and could be higher than those listed.

Under the plan, school districts could still assess property taxes if approved by voters for bonds or two other school-related funds. Should the state fail to provide full year-to-year funding to schools, school boards could also collect taxes, by a majority vote, to cover that shortfall.

If still unsatisfied, school boards could ask voters to approve higher rates. That would require 60% approval of a ballot issue in a statewide primary or general election, which comes every other year.

Rewriting the state’s education formula “to boost student outcomes” would not be tackled until the 2025 legislative session. Almost one-third of the Legislature will be brand-new next year.

Local city, county spending caps

Another component, which Jacobson said is critical, is spending caps on city and county governments, with few exceptions.

“I’ve said this from the beginning, that without spending caps, we’ll end up right back where we were before,” Jacobson said.

The Pillen model calls for a 0% increase in annual property tax collections in deflationary times or based on inflationary increases, as determined by the consumer price index each December for the previous 12 months.

Exceptions where local governments could seek increased property tax rates would include declared public emergencies, voter approved bonds and other voter-approved increases (which would also need 60% approval at a statewide primary or general election). The plan also calls for a “reasonable exemption” for public health and safety, which has not been defined.

New growth would be allowed, defined as the percentage increase in taxable property value due to annexations or property improvements from construction or other value-added services.

The plan would include state spending cuts

“To ensure this is a total tax reduction,” the plan continues, “a portion of financing will come from spending cuts at the state level.”

In a Friday column, Pillen said $360 million in state spending would be cut, which includes $200 million in the state’s general pocketbook and $160 million from the newly created Education Future Fund in the current fiscal year.

Savings have been identified by Pillen’s Cabinet and the ongoing efficiency study from the Utah-based Epiphany Associates, the draft states.

Other major funding will come from removing sales tax exemptions, raising “sin” taxes and using about $910 million from existing property tax programs, like homestead exemptions and property tax credits.

The target date for removing the exemptions is Oct. 1, with the Governor’s Office estimating about $663 million in new sales would be collected in the first nine months of implementation. In a full fiscal year, more than $1 billion would be collected.

Specific information on new “sin” taxes was not provided, though the governor has suggested raising cigarette taxes up $2 to $2.64 per pack and raising taxes on alcohol, vaping and more.

The plan doesn’t mention online sports betting, which the governor has said he’s open to, but does list new revenue from advertising services and cloud or other data-based software.

Pillen has said he would veto any proposal during the special session that includes legalizing and taxing marijuana.

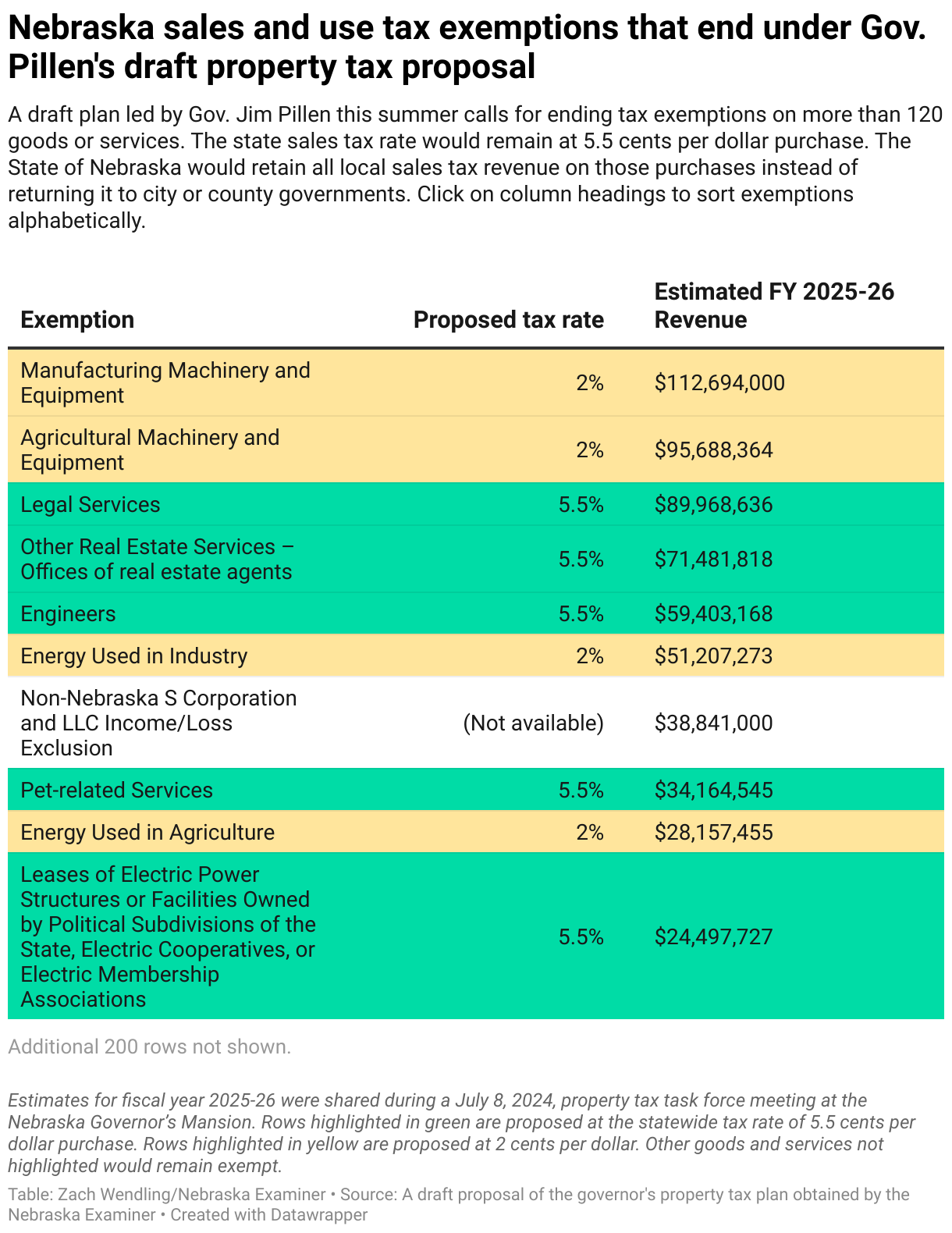

Proposed sales tax exemptions

The current statewide sales tax rate is 5.5 cents per dollar. Dakota County as well 261 cities or villages also levy local sales taxes between 0.5 cents and 2 cents, which are collected by the state and returned to local governments.

Under the draft plan, more than 120 goods and services would be added to the tax rolls.

The group has discussed the state keeping the local-levied portion on the new sales taxes, rather than returning that revenue to local governments as is done with all other purchases.

Some of the goods and services slated for the new tax system include animal grooming, debt counseling, custom meat slaughtering, home repair and maintenance, lobbying and consulting, motor vehicle repair, pinball and other mechanical amusements and veterinary services for pets.

Ibach said that the list of exemptions remains fluid and that some exemptions have already been dropped after last week’s meeting, including net wrap and certain catalysts, chemicals and materials used in manufacturing ethanol and its coproducts.

Ibach said she continues to take issue with removing ag or manufacturing sales tax exemptions because her district wouldn’t support them. She said there were some indications in the meetings that “sin” tax revenue may be well above projections, and she wants to consider that potential revenue before eliminating sales tax exemptions.

“The plan continues to be revised/updated with each task force meeting,” she said in a text.

The plan would also levy taxes on agricultural and manufacturing equipment or machinery and energy used in agriculture or industry, which are currently exempt.

However, those goods would be taxed at a new, lower rate: 2 cents per dollar purchase. To prevent “double taxation,” personal property taxes would be removed on any newly taxed goods.

In many cases, the suggested goods and services have never been on state sales tax rolls or were exempted over time through legislation.

What would remain exempt?

About 70 sales tax exemptions would remain, which could generate more than $5 billion if ended, according to the most recent Revenue Department estimates.

The most apparent is most food and groceries, medical equipment and medicine, and sales by religious organizations. Pillen had indicated all would remain exempt.

Also remaining tax-exempt would be: agricultural machinery repair and replacement parts, commercial artificial insemination, newspapers, laundromats, political campaign fundraisers, admissions to school events, public records and feminine hygiene products.

The two largest exempt categories would also remain: business components ($1.67 billion) and animal life whose products constitute food for human consumption or apparel ($1.18 billion).

While their broader categories are slated for new taxes, the following would remain exempt: coin-operated laundry; railroad rolling stock; special needs transportation services; offices for physicians, dentists, chiropractors, optometrists and mental health practitioners; substance abuse services; and other outpatient services.

‘A reverse Robin Hood scheme’

Riepe said in a text the plan benefits large net-worth property owners, both rural and residential, at the expense of middle- and lower-income renters who have not not seen the yet-to-be-publicized list of new sales taxes.

“If the Governor is so sure he’s right, why hasn’t he held one town hall in Lincoln or Omaha?” Riepe asked, pointing to the state’s two most populous cities.

“We need transparency/engagement and a legitimate process,” Riepe said in another text.

State Sens. Danielle Conrad of Lincoln and Julie Slama of Dunbar, who are not task force members, reviewed the proposal and both harshly criticized the contents.

Said Slama: “Pillen’s plan taxes the average Nebraskan to death, then taxes them again for burial.”

Conrad said despite Pillen’s “best efforts to hide the ball and keep citizens and senators in the dark,” his ideas have come to light. She said “our worst fears are being confirmed.”

“This plan is indeed nothing more than a reverse Robin Hood scheme representing perhaps an unprecedented tax increase and massive tax shift asking Nebraska families to pay more to benefit the largest wealthiest landowners in the state like himself, which is ridiculous,” Conrad said.

Conrad said Pillen’s plan is “unserious at best and dangerous at worst” and said Pillen should cancel the special session “because his so-called plan is dead on arrival.”

“If he pushes forward,” Conrad continued, “the Legislature will reject this nonsense and explore responsible realistic solutions to deliver for Nebraskans.”